Driven by nearly $49 billion in funding for new technologies like generative AI over the past three years, the San Francisco Bay Area maintains its rank as the top city across the globe for both innovation and talent, according to JLL’s latest Innovative Geographies report.

The research study states those investments were more than New York and Beijing combined during the same period. The San Francisco Bay Area outperformed most other markets on venture capital, research and development investment, productivity and talent breadth.

As was the case in previous years, the other top markets for innovation and talent included Boston (third), Tokyo, London, Seoul, Singapore, Shanghai and Paris. This year, Austin, Texas, placed eighth on the Top 15 list of top-performing cities for innovation and talent. Seattle came in 10th, followed by New York at 11th and Raleigh, N.C., rounding out the ranking in 15th place.

JLL’s third edition of the report looks at how innovations continue to influence real estate location and portfolio strategies, based on the dynamics of 108 cities globally. Ranked across a range of output, funding and talent indicators, JLL identified eight groups of cities across various innovation and talent concentrations to provide perspective on the rapidly evolving global landscape. Noting the pandemic caused the most severe correction on record, the report points out there are shifting demands from innovation-focused users across the industrial, office, lab and data center sectors. But there are also opportunities for occupiers, investors and public bodies.

Continuing migration

One of the report’s key findings is that migration of innovation and talent to affordable and lifestyle-centric cities continues, leading to sustained growth in secondary and tertiary markets. In the U.S., lower-cost cities like Austin have moved into the global tier of innovation hubs and a mid-sized city like Raleigh has registered marked improvements in both innovation and talent.

READ ALSO: AI Is a Silver Lining for the Office Market

Another mid-sized city, Las Vegas, is cited as a market likely to benefit from further spillover in the coming years with the potential to develop as an innovation cluster with gains in output, particularly patents and venture capital deployment. Nashville, Tenn., is called a secondary market that has greater affordability compared to larger markets enabling a higher rate of net migration along with increasing real estate demand and price growth. Miami is considered a destination for foreign direct investment and capital deployment at lower costs, fueling inbound migration and strong demand for real estate.

JLL notes that continued migration of talent, manufacturing and economic and corporate activity has pushed other U.S. cities like Austin, San Diego and Los Angeles into what it calls the “global builders” category. The report describes “global builders” as markets defined by mature, broad talent pools with high levels of overall output aided by extensive research and educational institutional presence. They tend to have lower real estate costs than “global leaders” like San Francisco but have similar demographic factors.

Other forces

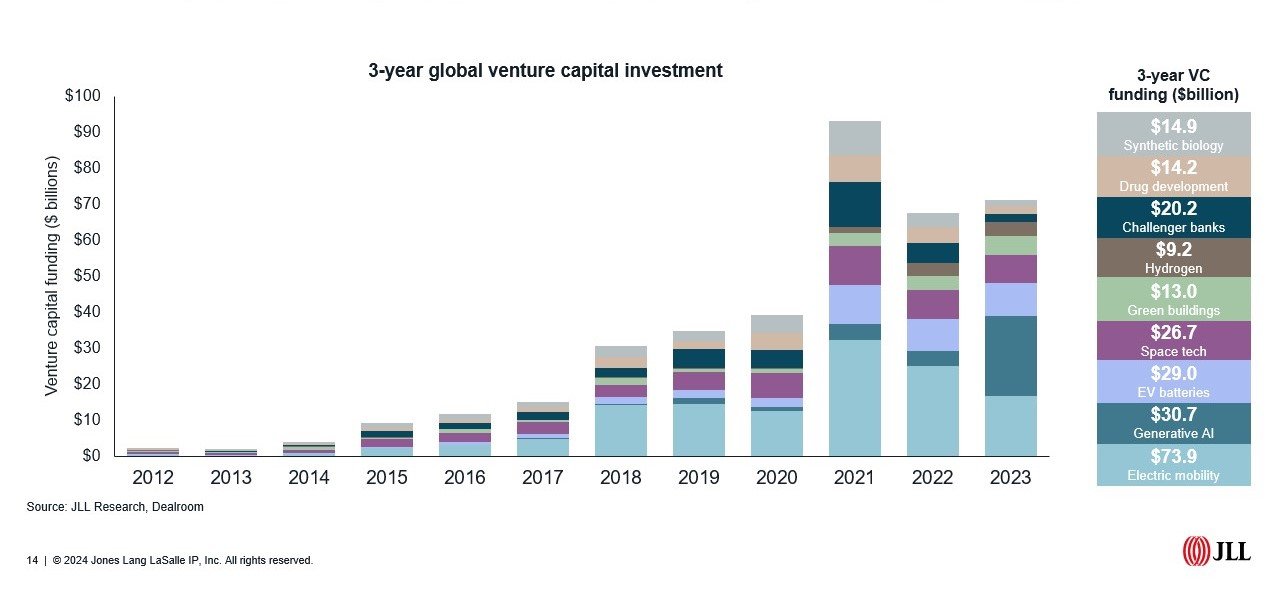

Throughout the next decade, market specialization, talent migration, sustainability goals and new technologies like AI will continue to drive commercial demand and reshape the built environment, according to the report. Injection of capital into newer technologies is driving market maturation and increasingly specialized clusters. JLL notes that generative AI has received $22.3 billion in venture capital in 2023. Adding in investments in areas such as electric mobility, batteries, green buildings and drug development, new innovation funding rose to $54.7 billion throughout 2023, more than doubling since 2020.

JLL states the geography of innovation is also being shaped by external geopolitical forces such as more aggressive trade and industrial policies that are incentivizing onshoring and increased domestic production of critical components.

The most visible impact in the U.S. has been the increase in plans for semiconductor manufacturing driven by funding from the CHIPS and Science Act. This realignment will place more emphasis on research and development as well as co-location of manufacturers with transportation and logistics nodes. JLL points to multibillion-dollar semiconductor or high-tech materials fabrication plants being built in or near metropolitan areas, particularly in the Phoenix and Columbus, Ohio, markets as examples.

Sustainability and efficiency standards also continue to drive innovation and alternative sectors will be critical in enabling many of the fastest-growing innovation geographies to cope with climate change impacts on real estate investments, including data centers. The report expects venture capital funding for green building technologies, which rose by 32 percent last year, to keep increasing.